Conceptualization of the back-ended risk premium

Many of the minerals considered critical for energy transition exhibit back-ended risk in project development caused by technical and non-technical risks occurring in the later stages of the project (six to eight years after the exploration starts)6,7,8. Examples of critical minerals that exhibit back-ended risk are bauxite, cobalt, lithium, graphite, niobium, nickel laterite, tungsten, scandium, rare earth, vanadium, and zinc. The existence of such back-ended risk means that investment is insufficient for these minerals to increase production in response to an increase in demand. This contrasts with the risk faced by other minerals—so-called front-ended risk minerals—such as gold, copper, and iron ore, for which the value of the project increases rapidly during the exploration stage. For these minerals, most of the investment needed for production occurs in the early stages of the project in response to an increase in demand.

In Fig. 1, we illustrate back-ended and front-ended risk project development and show how this relates to our proposed concept of the back-ended risk premium. The vertical axis represents the valuation (or share price) that the market places on the mineral project. The horizontal axis displays the different stages of development of the mining project (exploration, scoping, feasibility, development, and mining). At time \({T}_{1}\) the valuation (or share price) of front-ended risk minerals is \({V}_{2},\) which is much higher than the valuation of back-ended risk minerals (\({V}_{1}\)). Figure 2 shows that the valuations of back-ended and front-ended risk projects eventually converge after the development stage. The back-ended risk premium can be seen as the relative additional rate of return required by investors for back-ended minerals projects, relative to front-ended minerals projects, and in Fig. 1 is denoted by the gray-shaded area.

This figure illustrates the relationship between the value that investors attribute to the project at various stages of the development of the mining project. The red line represents this relationship for front-end minerals, while the blue line represents the corresponding relationship for back-end minerals. \({T}_{1}\) and \({T}_{2}\) denote the beginning and conclusion of the project development. \({V}_{1},\,{V}_{2}\) and \({V}_{3}\) are three alternative valuations attributed by investors to the project.

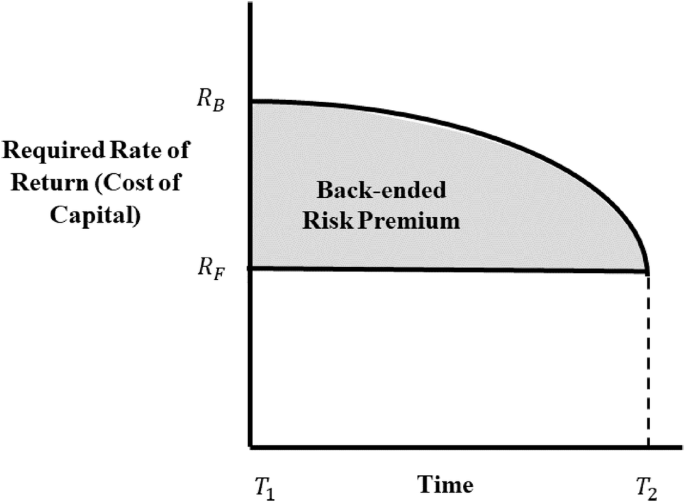

This figure illustrates the differences in the required rate of return to investors between front-ended and back-ended minerals. We define these differences as the back-ended risk premium. \({R}_{b}\) is the required rate of return for back-ended critical minerals and \({R}_{f}\) is the required rate of return for front-ended minerals. \({T}_{1}\) and \({T}_{2}\) denote the beginning and end of the project development.

Figure 1 suggests that for back-ended critical minerals, the value to shareholders only increases in the latter stages of the project development, meaning that investment (and production) will be lower than the market equilibrium requires. Figure 2 illustrates the difference in risk premium between front-ended and back-ended risk projects or the additional risk that investors would incur investing in back-ended minerals compared to front-ended minerals. The vertical axis represents the required rate of return by investors, and the horizontal axis denotes the time between \({T}_{1}\) and \({T}_{2}\) from Fig. 1. From this figure, we can infer the following:

-

Investors require a relatively larger return to be compensated by the back-ended risk premium.

-

The back-ended risk premium decreases as a function of time.

-

The back-ended risk premium is equal to the risk of front-ended minerals after \({T}_{2}\).

Risk premiums for critical minerals

Figure 3 presents the non-technical risk premium for each of the critical minerals for 2022. The measurement of the non-technical risk premium is described in the methods, Supplementary Information Section 2, and in the Supplementary Data. Each of the critical minerals exhibits a non-technical risk premium, relative to the front-ended non-critical mineral benchmark, consisting of coal, gold, and iron ore. The non-technical risk premium varies from rare earth elements (30.6%) to nickel (2.9%), with the average being 15.7%. The heterogeneity in non-technical risk between critical minerals largely reflects the geographical distribution of specific critical minerals, with those exhibiting higher non-technical risk concentrated in countries having less attractive investment environments. In Supplementary Fig. 3, we show these results are robust to including the only major front-ended critical mineral (copper) in addition to coal, gold and iron ore in the benchmark of front-ended minerals.

This figure represents the non-technical risk premium for 16 critical minerals relative to a front-ended minerals benchmark consisting of coal, gold, and iron ore for the period 2022. Details of the construction of this measure of the non-technical risk premium, data, and calculations are available in the methods, Supplementary Information, and Supplementary Data.

Figure 4 presents the technical risk premium for 14 critical minerals for which we have data. The measurement of the technical risk premium is described in the methods and Supplementary Information Section 3. Tin has the highest technical risk premium, while copper and antimony have a technical risk discount, relative to the non-critical mineral benchmark. The average technical risk premium across the 14 critical minerals is 18.4%.

This measure of the technical risk premium is based on six characteristics (crustal abundance, crustal concentration, ease of mining, ease of processing, criticality of use, and diversity of use). Details of the construction of this measure of the technical risk premium, data, and calculations are available in the methods, Supplementary Information, and Supplementary Data.

In Fig. 5, we present estimates of the total risk premium for the 13 critical minerals for which we have data on technical and non-technical risk. Rare earth elements, tin, manganese, tungsten, and zinc have the highest total risk premium. The only mineral showing a total risk premium discount is copper, reflecting its lower technical score relative to the benchmark.

Estimates of the back-ended risk premium

We provide conservative estimates of the cumulative back-ended risk premium depicted in Fig. 2 until 2035 under the IEA’s Sustainable Development Scenario (SDS) and Stated Policy Scenario (STEPS). STEPS is based on current policy settings, while SDS presents the best-case scenario for the clean energy transition. For each scenario, we calculate the total risk premium based on the weighted average of the market value of each critical mineral. Using the weighted average of the market value has the advantage that it considers differences in the relative importance of critical minerals to the clean energy transition. For the SDS, we calculate the total risk premium to be 32.5%, while for the STEPS the total risk premium is 31.6%.

Our estimates of the cumulative back-ended risk premium until 2035 are given in Fig. 6. The cumulative back-ended risk premium by 2035 ranges between USD 660 billion and USD 678 billion in the STEPS and SDS scenarios, respectively. Based on estimates described in the methods section, in our main analysis, we use 13.49% as the Weighted Average Cost of Capital (WACC) for the benchmark front-ended minerals. In Supplementary Figs. 4 and 5, as a sensitivity check on our main analysis, we alternatively assume that the WACC to calculate the back-ended risk premium is 12% or 16%. When the back-ended risk premium benchmark for front-ended minerals is estimated using a WACC of 12%, the cumulative back-ended risk premium decreases from USD 660-678 to USD 587-604, which can be considered a lower-bound estimate on the cumulative back-ended risk premium. In the upper bound case, when the back-ended risk premium benchmark for front-ended minerals is estimated based on 16%, the cumulative back-ended risk premium increases to the USD 775-804 billion range. This figure represents the additional cost of capital for back-ended projects and helps explain why investment in critical minerals is low even when long-term demand is high.

This figure presents the back-ended risk premium (BRP) for the Sustainable Development Scenario (SDS) and Stated Policies Scenario (STEPS), which are the two standard energy policy scenarios presented by the International Energy Agency.

Using AI to address the shortfall in critical minerals

A key feature of the AI revolution is that many roles will be automated, and machine learning procedures that heavily depend on capital will replace mundane labor tasks10. In a large survey of machine learning researchers, the consensus among respondents was that AI will outperform humans in many activities over the next decade11. The expected gains in productivity in critical minerals production that are hoped will meet the shortfall in supply will be in automation of the labor force and high-level machine intelligence, in which capital is the key component at all stages of the mining industry production process from exploration to extraction5.

The back-ended risk premium theory, presented above, implies that the cost of capital for back-ended minerals is higher than that for front-ended minerals. Our findings suggest that, on average, the WACC for front-ended minerals is 13.49%, whereas, for back-ended minerals, it is 4.26% and 4.44% higher, depending on the scenario (17.75% and 17.93%, respectively). Thus, in a capital-intensive industry in which productivity gains are expected to be made in AI developments, the increase in capital cost because of the back-ended risk premium is expected to be economically large, lowering productivity growth in the critical mineral sector.

In Fig. 7, we employ a production possibility frontier (PPF) to show how the back-ended risk premium affects the potential to increase productivity in back-ended critical minerals via AI. The initial curve shows the combination between capital (K) and labor (L) that is required to produce the maximum amount of minerals for a firm or economy, in which the factors of production are any combination along the PPF of \({L}_{1}\) and \({K}_{1}\). The green line represents a potential increase in productivity due to AI-technologies which requires more investment in capital (technology). Here capital increases from \({K}_{1}\) to \({K}_{2}\) and the initial PPF rotates outwards and to the right to \({L}_{1}\) and \({K}_{2}\). The broken blue line represents the new PPF when the back-ended risk premium is considered. The blue line shows that some of the gains in production made by development in AI-technologies is lost due to the higher cost of capital, reflecting the back-ended risk premium. The loss in production is represented by the move from \({K}_{2}\) to \({K}_{3}\).

\({K}_{1}\) represents the initial level of capital at the initial Production Possibility Frontier (PPF), \({K}_{2}\) illustrates the level of capital after an increase in productivity due to technological advances in artificial intelligence in mining and \({K}_{3}\) denotes the level of capital considering the impact of the back-ended risk premium. \({L}_{1}\) is the amount of labor required for the three PPFs presented.

The analysis in Fig. 7 may be overly pessimistic. It overlooks the potential for AI to potentially reduce the back-ended risk premium by reducing the cost of capital for critical minerals mining projects. AI could reduce the back-ended risk premium by reducing the duration of mining projects and reducing the required rate of return on investment. We next consider the different ways in which AI could reduce the duration of mining projects and the required rate of return on investment, although we caution the reader that AI also has limitations, which we outline below. The potential benefits of AI for reducing the back-ended risk premium should be seen in light of those limitations.

There are multiple ways through which AI could potentially reduce the time from exploration to extraction in mining projects. One way is through improved mineral mapping. AI techniques, such as drone-based photogrammetry and remote sensing, can be used to automate the process of mineral mapping, making it possible to predict with greater accuracy regions with higher potential for new deposits12,13,14,15. Deep learning algorithms have been shown to provide a very high-level of accuracy in image recognition, which can be used for mineral resource mapping with surface and sub-surface image data12.

Supply-side risk stemming from the geographical concentration of critical minerals in a few countries has led to increased focus on the role of AI in detecting unconventional deposits of critical minerals in situ geological deposits of oil, gas, or coal mineral deposits from secondary by-products of anthropogenic processes16,17,18,19. An advantage AI has in such contexts is that a large amount of data has been collected through fossil fuel exploration on such geological deposits, which is well suited to machine learning20.

A second way in which AI could reduce the risk associated with duration from exploration to extraction is by making it possible to more accurately calculate the duration of the extraction period of the mine14. One of the most important risks for all mining projects relates to the orebody itself – ie. there is significant uncertainty about mineral resources21,22. One specific contributor to uncertainty being higher for critical minerals than conventional minerals in this early stage is that there are relatively few sources of data on critical mineral reserves. A second point of difference is that critical minerals are recovered as by-products from refining other metals. This means that the metal supply responds not only to the price of the by-product metal but also to the price of the host metal, which affects reserve estimates23. Uncertainty about the potential to recover critical minerals from mine waste, such as tailings, is particularly acute24. A third important way in which critical minerals differ from fossil fuels is that the former can be recycled, although the implications of recycling on future reserves is difficult to quantify, adding to uncertainty about available reserves23. Mining and extraction methods are dictated by the geology of the orebody or orebodies. AI can be used to provide a more accurate depiction of the geology of the orebody and its associated uncertainties25. Several AI methods have been developed to predict the grade and recovery of mineral deposits, reducing the associated technical risk26.

A third avenue for reducing the time from exploration to extraction is through employing AI to improve mining productivity. Risks associated with drilling and blasting performance depend on proper rock fragmentation. AI can be used to predict rock fragmentation and provide real-time evaluation of drilling performance that improves efficiency12. Automated drilling can be fitted with sensors that target specific ores; hence, reducing exploration time27.

AI can also be used to reduce the required rate of return on investment in two main ways. One way is through reducing uncertainty with the risk of a blowout in the cost, which is particularly important for back-ended minerals given that the initial cost of capital is higher than for front-ended minerals. For example, AI can be used to forecast the capital cost of open-pit mining projects28. Equipment selection is the most important phase during mine planning. The capital investment in selecting the right equipment represents a major risk. AI algorithms can be used to reduce the risk with equipment selection12. Once the mine is in operation, AI can be used for predictive maintenance and management of equipment, minimizing repairs27.

AI could also reduce the required rate of return on back-ended projects through reducing the risk, particularly environmental risks, associated with such projects. There is evidence which shows that AI algorithms can be effective in reducing disasters and environmental hazards associated with energy mining29. This is particularly important in the case of some key back-ended critical minerals, such as cobalt and lithium.

According to the U.S Geological Survey, more than 50% of the global proven lithium reserves are concentrated in the lithium triangle between Chile, Bolivia, and Argentina. Lithium in this region is mined from salt deserts or so-called salars30. Extracting lithium from salars has generated long-term environmental damage, with locals complaining that lithium mining has increased the prevalence of droughts, threatening livestock farming and drying out vegetation31. About half of the proven reserves of cobalt are located in Congo Kinshasa. Weak institutions, corruption, and conflict in the region exacerbate environmental risks associated with mining Cobalt. The technical risks associated with artisanal mining practices in Congo Kinshaha have caused environmental degradation, including deforestation, soil erosion, water pollution, and biodiversity loss. Unregulated mining activities, using mercury and other chemicals, and inadequate waste management practices can negatively affect ecosystems and local communities in the long term32.

The potential impact of AI on the rate of return and duration of the project are illustrated in Figs. 8 and 9, respectively. In Fig. 8, the potential impact of progress in AI on reducing the risk/rate on the back-ended risk premium is represented by the shift from \({R}_{B}\) to \({R}_{{AI}}\) while the volume of this reduction is represented by the area between the blue and green lines. Formally:

$$\int\limits_{{R}_{F}}^{{R}_{B}}F\left({R}_{B}\right)-\int\limits_{{R}_{{AI}}}^{{R}_{B}}F\left({R}_{{AI}}\right)\,={BRP\; reduction\; by\; AI}({risk}/{rate})\,$$

\({R}_{B}\) represents the required rate of return for back-ended critical minerals, \({R}_{F}\) denotes the required rate of return for front-ended minerals, and \({R}_{{AI}}\) indicates the required rate of return after considering advancements in artificial intelligence technology. \({{T}}_{1}\) and \({T}_{2}\) denote the start and end times of the project developments, respectively. \({f \left(\right. R}_{b}\)) and \({f\left(\right.R}_{{AI}}\)) are functions of \({R}_{B}\) and, \({R}_{{AI}}\), respectively.

\({R}_{B}\) represents the required rate of return for back-ended critical minerals, and \({R}_{F}\) denotes the required rate of return for front-ended minerals. \({T}_{1}{{{\rm{and}}}}{T}_{B}\) denote the start and end times of the project developments, respective\({ly}.\,{T}_{{AI}}\,\) indicates the required rate of return after considering advancements in artificial intelligence technology. \({f\left(\right. T}_{B}\)) and \({f\left(\right. T}_{{AI}}\)) are functions of \({T}_{B}\) and, \({T}_{{AI}}\), respectively.

In Fig. 9, the impact of AI progress on reducing the mining project time is represented by the shift from \({T}_{B}\) to \({T}_{{AI}}\) (the area between the blue and the green lines represents the volume). Formally:

$$\int\limits_{{T}_{0}}^{{T}_{B}}F\left({T}_{B}\right)-\int\limits_{{T}_{{AI}}}^{{T}_{B}}F\left({T}_{{AI}}\right)\,={BRP\; reduction\; by\; AI}({time})\,$$

In Fig. 10, we demonstrate the effect of lowering the rate of the back-ended risk premium and a reduction in the duration of mining projects because of advancements in AI technology. For simplicity, we assume a 50% reduction in risk. Since our estimates are proportional, readers can infer proportional reductions at different percentages. A 50% reduction in risk resulting from AI improvements leads to a corresponding decrease in the back-ended risk premium, falling within the range USD 330 (STEPS) to USD 341 billion, while a 50% shortening of project duration resulting from AI improvements leads to a corresponding decrease in the back-ended risk premium, falling within the range USD 330 billion (STEPS) to USD 334 billion (SDS).

This figure describes the cumulative effect of artificial intelligence on the back-ended risk premium (BRP) for the Sustainable Development Scenario (SDS) and Stated Policy Scenario (STEPS), which are the two standard energy policy scenarios presented by the IEA. a shows the cumulative impact of a 50% reduction in the risk rate. b shows the cumulative impact of a 50% reduction in project duration.

Investment in AI can eliminate the negative impact on the back-ended risk premium on investment in and production of critical minerals, which is key to achieving net zero. Various combinations of reductions in the risk/return associated with back-ended projects, as well as the duration of mining project time, may achieve a zero back-ended risk premium. Again, conclusions about the potential for AI to address the back-ended risk premium are subject to AI’s limitations outlined below.

Subject to these limitations, the implication of this result for the energy transition is that an immediate large-scale direct investment in critical minerals’ projects by governments between USD 660 and USD 678 billion is needed over the next decade. This amount is consistent with the shortage in investment estimated by the IEA2. The back-ended risk premium is an additional cost to achieve net zero 2050 that policymakers, thus far, have not considered when estimating the shortfall in investment.

What if meeting carbon net zero by 2050 is not possible?

Some studies have posited that, given existing mining constraints and known reserves of critical minerals needed for clean energy transition, replacing existing fossil fuel sources for energy requirements with renewable alternatives will not be possible by 2050. For example, one study finds that of 29 necessary metals in the lifecycle of renewable energy technologies, known reserves of eight metals might be depleted by 205033. Another study presents several scenarios for transition to carbon net zero, concluding that ultimately, global reserves of cobalt, nickel, and lithium may not be enough to resource the number of batteries needed to power the electric vehicles needed for clean energy transition34.

What does this mean for the back-ended risk premium and AI’s potential mitigation of this risk premium? Our interpretation is that the conclusion from such studies reinforces the importance of attracting investment in back-ended critical minerals to reduce the expected shortfall to realize the clean energy transition. It also highlights the importance of investment in AI applications in development and exploration to reduce the duration of mining projects and reduce the required rate of return on investment. Micheaux suggests that if existing critical mineral reserves are not sufficient to resource clean energy transition, a new social contract may be required that limits energy demand34. A pessimistic conclusion from this might be that if commitment to energy transition by 2050 is ignored this might erode the motivation for global support for net zero emissions from governments and lending agencies. In such circumstances, other solutions would need to be found, and financing investment in back-ended critical minerals would be less important, making the back-ended risk premium less important. However, this is unlikely. Given the global recognition of the threat posed by climate change, it is very unlikely that commitment to clean energy transition will be eroded even if meeting 2050 targets proves not to be feasible. If commitment to the clean energy transition did look like faltering, reducing expected demand for critical minerals, the added uncertainty would increase the back-ended risk premium by increasing the required rate of return on investment35. In this sense, the potential that political commitment to clean energy transition, broadly defined, could wane is a non-technical risk, which increases the uncertainty associated with investing in critical minerals, meaning investors require a higher rate of return. This applies a fortiori to critical minerals that have a high likelihood of running out before 2050. All things equal, the back-ended risk premium for these critical minerals will be higher because the uncertainty about their utility to the clean energy transition is particularly acute. However, it is important to note that the likelihood of a given mineral running out before 2050 is just one non-technical risk among many. Of the eight minerals that Moreau et al.33 conclude might be depleted by 2050, we consider four in this study (cobalt, nickel, tin, and zinc). It is noteworthy that each of these four critical minerals has a relatively low non-technical risk premium (see Fig. 3). More generally, most likely, even if critical minerals do not provide the full solution to resourcing the clean energy transition, they will at least still provide some of the solution, in conjunction with other initiatives, and further investment in critical minerals will be needed to facilitate this.

Limitations on AI as a solution to the back-ended risk premium

We show that improvements in AI have the potential to reduce the back-ended risk premium. However, AI is going to require further investment to ensure the required gains and there is uncertainty about whether and when the benefits of AI will be realized. While it is often touted that AI will lead to improvements in productivity in mining and a reduction in mining project risks, there is a distribution of AI applications in mining and mineral processing in terms of maturity on the Gartner hype cycle for developing new technologies36, with many technologies still early on the curve (especially at ‘peak of inflated expectations’). AI has experienced a number of ‘hype cycles’ in which unrealistic expectations have preceded periods of under-delivery, funding cuts, and slowdowns in investment in R&D37.

Recent meta-studies have also revealed a worrying tendency for overly optimistic AI performance reporting, due to data leakage and lack of reproducibility38,39. Messeri and Crokett argue that “AI solutions can exploit our cognitive limitations, making us vulnerable to illusions of understanding in which we believe we understand more about the world than we actually do”40. AI faces specific challenges in mining and mineral processing projects. One of the main challenges facing the mining sector in exploiting the potential of AI is addressing the skills gap, with many workers requiring reskilling or upskilling to take advantage of AI4,27,41.

A second set of challenges facing AI in mining studies is the lack of high-quality training data14,37,42. The application of AI has been limited by the use of small datasets26,42. Cost forecasting applications are typically based on relatively few data points4. Given that the exploration of critical minerals is relatively new and that there are relatively few critical minerals (and particularly back-ended critical minerals), the lack of databases and experimental data to train and test AI models is particularly acute.

A third related problem is that mining operations often take place in remote locations making access difficult. Abrasive materials, dust, and humidity that are commonplace in mines do not create a congenial environment for the deployment of digital technologies. In underground mining, installed sensors need to be resistant not only to dust and humidity but also to blasting that can damage the senses. Transmitting the data can be problematic due to the limited bandwidth of communication networks employed in underground and open-pit mining. Connectivity can be particularly weak and unstable in deep mine sites27. This makes the storage and transmission of useful data challenging43.

Policy recommendations

The main problem that back-ended critical minerals has is that they provide lower value to investors during the initial stages of project development and exploration, due to technical and non-technical risks. Our analysis suggests that the most important stages to invest in AI to reduce the back-end premium is in applications between exploration and development.

It is essential to highlight that investing in mining in these stages is distinct from investing in AI made by governments, the private sector, and global funding agencies in general. In 2021–2022, the United States Federal Government, as the global leader in AI investment, spent USD 3.3 billion on AI, while worldwide private sector investment in AI was USD 91.9 billion44. In comparison, mining companies were expected to spend just USD 218 million on AI globally in 202445 with only a fraction of this invested in AI in supporting development and exploration in back-ended critical minerals.

Our suggestions below for areas of investment in AI apply to governments, the private sector, and lending agencies such as the World Bank and IMF. The argument for government investment in AI applications is that it is broad-based, and the benefits of technical breakthroughs can extend beyond a single firm or sector. However, there is also a strong argument for the critical minerals sector to invest in AI to reduce the back-ended risk premium, given it is in their interests to attract investment. Improvements in AI in the development and exploration phase can reduce the back-ended risk premium by both reducing the duration of the project and reducing the required rate of return on investment.

Most AI applications in mining have focused on the development and exploration phase, which is where AI is particularly useful in mitigating technical risks4,15. One specific AI application in which governments and mining companies could invest is in data-driven prospectivity modeling, where random forest46 and extreme learning machine models47 have been used to more accurately predict recovery rates and reduce the time from exploration to extraction. A second related AI application is in mineral mapping in which drilling sensors, geophysical-geochemical-remote sensing surveys, and 3D geological modeling can be used to more accurately predict locations with the most potential for mineral deposits48,49,50,51.

A third area for potential investment would be in AI methods, such as artificial neural networks52 and extreme learning models53, to predict the grade and recovery of mineral deposits. A fourth promising area for investment in AI is in the recovery of critical minerals from mining waste. AI has proved particularly useful in improving secondary recovery approaches, such as adsorption54,55.

Lithium extraction in Chile, Bolivia, and Argentina is plagued by water scarcity. Scarcity of water and water management is one of the main challenges of mineral processing plants that lead to delays56. Automated ‘dry’ or water-savvy sensing AI techniques can be employed to minimize these risks25. The benefits of using critical minerals, such as lithium, to facilitate the clean energy transition will be muted if they are extracted in an environmentally unfriendly way. More generally, investment in AI-powered environmental monitoring systems, such as smart earth technologies, could help mitigate the impact of minerals such as cobalt and lithium on the environment by detecting and addressing pollution in real time56. One of the biggest obstacles to the successful adoption of AI in addressing back-ended risk is the lack of data. Creating publicly available material datasets that can be used as a source of model training and testing is a common recommendation for further AI applications in mining42. Given the public goods nature of having open access material datasets, this is one area in which governments and international lending agencies could invest.