Investment approach

Investing in high quality companies

CLDN’s approach incorporates three investment strategies, each of which is fundamentally doing the same thing – identifying and backing high quality and growing companies, while seeking to manage company specific risks through diversification, both by company, market and geography and investing time in understanding the companies and what drives returns through extensive due diligence – but in different areas of the market.

‘Time is our friend’

CLDN believes in the power of compounding returns over long periods of time. Taking a long-term view and being patient have been key to its success. As a self-managed trust, CLDN is not constrained by a need to meet short-term performance objectives or comply with fixed-life fund cycles. The team is focused solely on CLDN’s success, incentivised in such a way as to be aligned with shareholders, and is not distracted by running outside money or the need to fundraise.

CLDN has access to revolving credit facilities for working capital purposes but does not have any permanent debt. Investments are funded off its balance sheet.

Accomplishing CLDN’s objectives requires a great team of people and a willingness to tap into outside expertise when appropriate.

Strategy is set by the CEO and the board has an oversight function

Everything is managed from one office. Strategy is set by the CEO with support from the executive team. The board provides oversight, but it is not involved in day-to-day decisions. However, it will sign off material investment decisions, such as a new investment or realisation in the private capital portfolio.

Day-to-day investment decisions are signed off by an investment committee

All investment decisions are signed off by an investment committee made up of CEO Mat Masters, CFO Rob Memmott, company secretary Richard Webster, and the team heads – Jamie Cayzer Colvin (head of funds), Tom Leader (head of private capital), Ben Archer (co-head of public companies), and Alan Murran (co-head of public companies).

They find that debating the merits of each investment decision promotes a culture of long term ownership, in line with CLDN’s overall ethos.

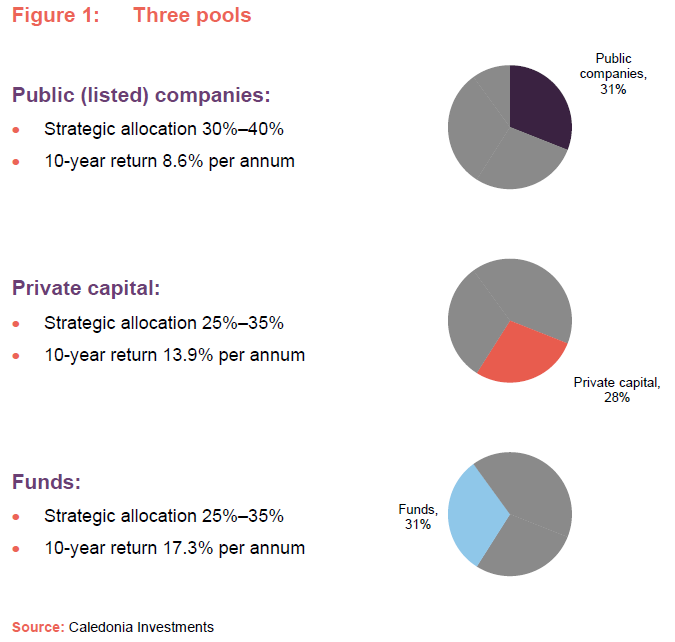

Three pools

CLDN’s capital is invested across three pools – each has a strategic allocation and target return. The three investment strategies deliberately address large markets. which CLDN expect will offer attractive long-term opportunities.

Public companies

Capital and income pools of public companies

The public companies allocation is run by a single team and is not managed to any benchmark. The strategic allocation to this part of the portfolio has been set at 30%–40%, but this pool of assets is further subdivided into a capital portfolio – headed up by Alan Murran – and an income portfolio – headed up by Ben Archer. Altogether, they hold about 30 stocks.

High quality, well-understood businesses

In both cases, these are global portfolios of high-quality businesses that the team feels that it has a good understanding of. These companies should have underlying growth and pricing power. Companies with little trading history, unprofitable companies, and recent IPOs are discounted. There is also a general aversion to banks and companies sensitive to commodity price fluctuations.

Targeting 10% a year on the capital portfolio and 7% a year on the income portfolio

The portfolios are invested to achieve a total return target of 10% a year on the capital portfolio and 7% a year on the income portfolio.

The capital portfolio is unconstrained. Given the importance ascribed to the quality of these businesses, many will pay a dividend, and this part of the portfolio makes a meaningful contribution to the trust’s revenue account.

The income portfolio, valued at £251m (currently 26.5% of the public companies portfolio) provides a reliable income stream to cover a portion of CLDN’s cost base and dividend.

Think about what might go wrong

The team does a great deal of due diligence on potential investments. The outlook for these companies is considered over the long term and emphasis is placed on determining what might go wrong with their investment thesis. Companies that appear to be good at optimising returns on capital are favoured. They should have robust balance sheets.

Do your research and be nimble when the chance arises

The team will form a view of an appropriate valuation for a stock through extensive due diligence and financial modelling. Nevertheless, periods of stock market volatility – such as the March 2020 COVID panic – can provide an opportunity to invest at attractive prices (as we show when discussing Oracle on page 15 and Watsco on page 16). It is important that they have done the work ahead of time and then can be nimble when the chance arises.

When stocks get more expensive, they are reassessed against the 10% per annum long-term target. The team may trim or add to positions on market volatility, but turnover is generally low.

3.5% yield target on cost to support CLDN’s progressive dividend policy

Recognising that higher dividend yields are often associated with riskier businesses, the yield threshold for a stock to be considered for inclusion within the income portfolio is now 3.5% on cost (down from 4.5%). The team wants to hang onto good quality businesses, and so any income stock that re-rates so that its running yield falls below this level may be retained within the portfolio. Given the target of growing investors’ income in real terms, it is important that these stocks offer good dividend growth prospects. However, the team takes a portfolio approach, including a mix of higher-yielding lower growth stocks as well as lower-yielding but faster-growth companies.

(Commentary on the recent performance of this pool is provided on pages 19 and 20).

Private capital

Focused portfolio of private companies

This part of the portfolio is invested in a target portfolio of six to eight companies with the aim of generating a total return target of 14% a year and a 2.5% yield on cost. The strategic allocation to this area is 25%–35%. However, it is currently towards the lower end of that range following the sale of 7IM (see page 8).

The 10-strong private capital team is led by Tom Leader. It is focused on origination, valuation and working to support value creation within investee companies. Unlike traditional private equity investors, the long-term focus of CLDN means that the team have a buy-to-own philosophy rather than buy-to-sell.

The private capital allocation is composed of direct investments focused on high-quality, mainly-UK headquartered, mid-market companies.

CLDN partners with management to drive improvements; leverage used conservatively

Typically, CLDN will invest £50m–£150m in these businesses for a controlling stake (although there are some minority positions within the portfolio). CLDN sees itself as partnering with these companies. Value is created by improving the underlying business rather than financial engineering.

Leverage (borrowing) is used conservatively, typically in a range of 2x–2.5x EBITDA. That makes this part of the portfolio much less sensitive to interest rates and helps facilitate the payment of dividends.

Good quality businesses with a path to improving profitability

Given the income requirement and CLDN’s conservative approach, target companies must be good-quality, EBITDA-positive (they are unlikely to buy a loss-making company), and have a clear path to increasing profitability. When assessing potential investments, maintenance capex is factored into their deliberations. CLDN tends to avoid capital-hungry businesses and is happy to support sensible accretive bolt on acquisitions, but is unlikely to seek out a buy-and-build strategy (7IM is a good example of this – see page 8).

CLDN is wholly aligned with the underlying management teams

CLDN likes to back good management teams, but is happy to make changes where necessary, for succession reasons for example, and can tap into its network to help source talent. CLDN seeks to align with management by investing in the same ordinary equity as them. In addition, as an evergreen fund, CLDN can be a genuine long-term backer of these businesses, and that helps build trust.

CLDN works with the management team, not looking to interfere with the day-to-day running of the company, but rather to provide a strategic partner and, when needed, capital for investment and acquisitions.

Realisations

Unlike a typical private equity investor, there is no fixed timeframe for realising these assets and CLDN will happily continue to hold them as long as it sees long-term growth potential. However, all of these investments are for sale at the right price.

As one example, Deep Sea Electronics – a business that CLDN bought in 2018 for equity of £117.2m and short-term debt of £50m that was subsequently repaid – was one that the team was happy to hold for the long term. However, Genarac Holdings – a US strategic buyer – was keen to acquire the company and CLDN sold its stake for net proceeds of £242.2m in 2021, making a return of 2.0x in three years.

There is no proscribed upper limit for the size of a successful investment within the portfolio, but CLDN are conscious of single asset risk.

Seven Investment Management

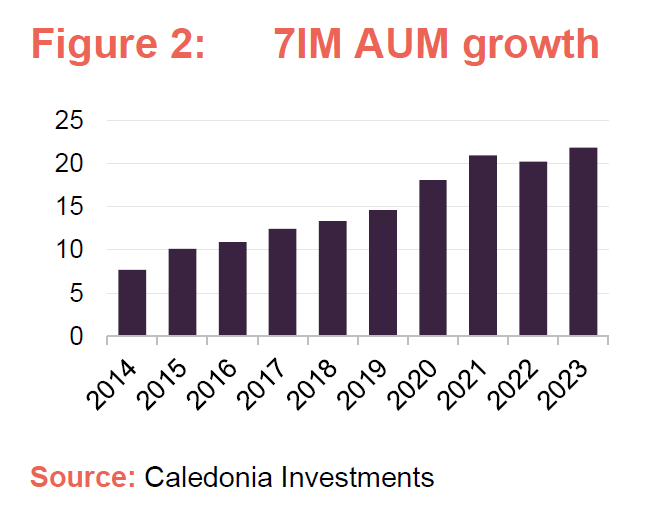

Seven Investment Management was a recent success. In 2023, CLDN’s stake in that business was sold to Ontario Teachers’ Penson Plan Board for £255m, crystallising a return of 2.3x on cost and a 15% IRR.

CLDN acquired a 94% stake in the business for £74m in September 2015 and topped this up with £54m of follow-on capital, although this was offset by £42m of dividends.

CLDN’s investment thesis for long term ownership was to expand direct to consumer distribution, invest in people and operations and management succession. A new CEO was appointed in 2019 and a new chair in 2020.

7IM implemented a strategic shift under CLDN’s ownership, expanding its reach to retail customers, with a shift to a ‘platform led’ wealth manager model.

7IM’s assets under management grew from £7.7bn in 2014 to £21.8bn at the end of the third quarter of 2023 (Q3 2023). Much of this was organic, however 7IM also acquired Tcam in 2018, Partners Wealth Management and Find a Wealth Manager in 2020, and Amicus Wealth in 2023.

(Commentary on the recent performance of this pool is provided on page 20).

Private equity funds

Funds provide exposure to things that the team could not do on its own

The strategic allocation to this area is 25%–35% and the total return target is 12.5% per annum. The funds allocation provides diversified long term returns in geographic markets that counterbalance CLDN’s quoted equity and UK-centric private capital investments. This part of CLDN’s portfolio covers about 74 funds (including some funds of funds), managed by 42 managers, with over 600 underlying companies.

The allocation is split currently between North America (59%) and Asia (41%). Globally, market activity has slowed over the last 18 months, although there was a pick-up in North America in the first quarter of 2024. The team is expecting relatively depressed levels of activity in Asia to continue for a while yet.

CLDN wants to see evidence that the underlying General Partner’s (GP) approach is working before making an investment with them. Usually, therefore, CLDN will typically not invest until the GP is launching its second or third fund. The team does not tend to invest in first time funds, unless they are backing a team that has spun out from a manager they know well.

Valuations are conservative – there is no benefit to write them up ahead of realisation

There is no benefit to the GPs to writing up valuations (because fees are based on committed capital and crystallised capital gains) and so there is often a big jump in the value of a position on realisation.

At end March 2024, CLDN had outstanding commitments of £377m that it expected to be drawn over three to four years. That was balanced against cash of £227m and CLDN’s £250m undrawn credit facility. CLDN says that it expects a number of its US managers to be fundraising over the next 12-18 months, as broader market conditions for exits in this market improve.

North America

US lower mid-market buyouts, a hard to access part of the market for UK-based investors

The North American exposure is to lower-mid-market buyouts, a part of the market that is hard to access for UK-based investors. Often, they are the only European investor in these funds, and have an advisory board seat for 80% of the funds. There is less competition for deals in this part of the market and typically this represents the first institutional money being invested in these companies. The GPs provide knowledge, resources, and capital. They may also add some leverage. Exits tend to be to strategic buyers alongside mid-market private equity players.

Typically, CLDN is making primary investments into four or five new LPs each year and can also participate in the secondary market. Three of these deals will be with GPs that they have backed before, and the balance will be with new GPs.

The team considered whether it should get exposure through co-investments, but decided that this did not make sense from a risk perspective in its chosen area of lower mid-market.

The weighted average life (time elapsed since first investment) of CLDN’s North American primary fund investments is about 4.0 years. Most private equity limited partnership (LP) structures are established with 10-year lives and will typically look to hold investments for between four and seven years. Hence a weighted average life of 4.0 years might suggest that these funds contain a number of relatively mature investments.

New Heritage Capital

To illustrate the approach, CLDN recently provided investors with more information on its investments with New Heritage Capital, a mid-market (enterprise value of $50m–$200m) buyout firm based in Boston with a focus on business services, healthcare services and specialised manufacturing.

It aims to take control of and then add value to the companies that it invests in but likes the family/founder owners of these businesses to retain an investment. Typically, New Heritage Capital is the first institutional investor in these companies.

The first New Heritage Capital fund was launched in 2006. CLDN identified it as a potential partner in 2015 but made its first commitment of $20m to New Heritage Capital’s $260m Fund III in 2019 and then a further $30m to its $438m Fund IV in 2024. Each of these funds tends to make 10–12 investments at a rate of about 1–3 investments per year.

As at 31 March 2024, the Fund III investment was valued at 2.0x CLDN’s investment. Exits achieved by 31 March 2024 included Revela Foods and Carnegie at a premium to NAV.

Asia

In Asia, CLDN holds funds that give it exposure to buyout (through funds-of-funds), growth, and venture capital in non-cyclical, new economy sectors. These sectors, such as healthcare and technology, tend to benefit from underlying demographic trends. The end markets for some of these products and services may be outside Asia, in the US, for example.

While these are investments in relatively young, growing companies, CLDN’s focus is on companies with proven business models.

Breaking down the 41% of the fund’s pool that was invested in Asia at end .March 2024, 23% was in directly-owned funds and18% is invested through fund of funds providers such as Asia Alternatives, Axiom, and Unicorn.

The team observes that, as the private equity market is less mature in Asia, exit opportunities are provided mainly by IPOs and trade sales. Exits have been impacted by market volatility and geopolitical uncertainty. Consequently, the CLDN team feels that the pace of distributions could take longer to improve in Asia.

The weighted average life of CLDN’s Asian investments is about 5.1 years.

(Commentary on the recent performance of this pool is provided on page 20).

Environmental, social, and governance (ESG)

CLDN is a responsible investor and does not seek to profit from things that do damage to the environment or society without a strategy for change. It does not operate a list of banned sectors or companies; rather, investments are considered individually and an assessment of ESG factors is built into all stages of the investment process. A responsible investment/responsible corporate working group chaired by the CEO oversees CLDN’s efforts in this area.

Within public companies, the CLDN team exercises its voting rights at shareholder meetings of portfolio companies. Every voting decision is considered by the team rather than being outsourced to a third party.

The approach naturally excludes many polluting industries and consequently the scope 1 and 2 carbon emissions of CLDN’s public companies allocation are well below those of the MSCI World Index.

Within the private capital allocation, where CLDN is represented on the boards of these companies, CLDN monitors a range of key performance indicators and requires the companies to document progress against these. The team finds that this discipline adds value on exit.

Within the funds allocation, CLDN maps and monitors ESG matters into due diligence, portfolio monitoring and General Partner engagement.

CLDN is seeking to reduce its own net greenhouse gas emissions and wants companies that are significant emitters to reduce their emissions. It expects the businesses in which it invests to target net zero emissions by 2050.